Rathke

Investment Summary

Hexcel (NYSE:HXL) is a leading manufacturer of advanced composite materials (carbon fiber) for commercial aerospace, defense, and industrial end markets. They operate globally with manufacturing facilities across the Americas, Europe, Asia, India, and Africa. Hexcel holds the #1 position in aerospace composite sales and production capacity and carries a wide range of trademark products. Three factors drive Hexcel’s value. 1) its ability to sell composite materials to commercial aerospace OEMs (mainly Airbus (OTCPK:EADSY) and Boeing (BA)); 2) its ability to win government contracts; and 3) its ability to manage its operational cost structure.

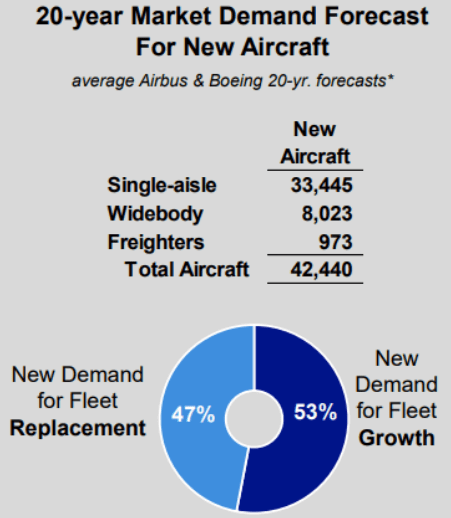

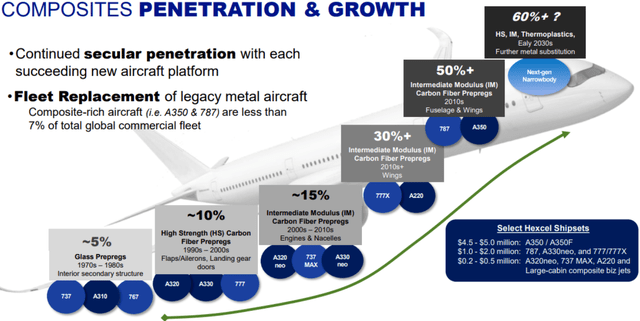

Currently, only 7% of the global commercial aircraft fleet consists of composite-rich planes (carbon fiber frames), with the majority consisting of an aluminum frames. This creates a secular growth opportunity as aircraft fleets are replaced with more composite-rich shipsets to improve fuel efficiency and lower life cycle costs. Over the next 20 years, Airbus and Boeing expect 42,440 aircraft deliveries, a majority of which should contain incrementally higher carbon fiber bases. In the near term, deliveries remain challenged due to issues across the supply chain and at Boeing. Positively, Hexcel has more exposure to Airbus (39% of revenue) than Boeing (15% of revenue), giving Hexcel an advantageous position to pick up expected Airbus delivery ramps in 2025. This is all supported by Hexcel’s above production capacity levels from pre-covid investments (likely at ~75% of capacity). Together, this should drive >100% FCF conversion, and record levels of share repurchases.

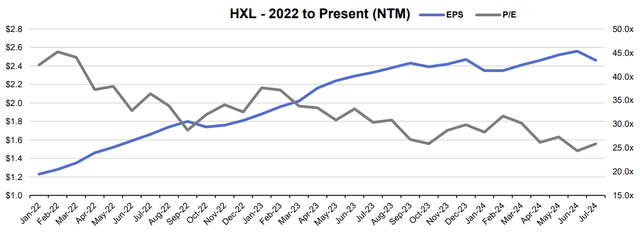

All in, Hexcel is well positioned in a secular growth market to drive long-term, above-average EPS growth and multiple expansion. On an NTM basis, Hexcel is priced on trough earnings of $2.37, demanding a ~25x multiple. Looking out to 2026, when deliveries are expected to normalize, the street expects earnings of $3.40 implying a ~27% CAGR. Assuming already in place capacity drives higher-than-expected margins, and investors recognize long-term industry tailwinds, Hexcel could see a 30% EPS CAGR and 25x multiple. This implies EPS of $3.55 and a share price of $89 by 2026, or ~16% annualized upside.

Company 10-k

Company Overview

Hexcel operates through two segments, Composite Materials (82% of revenue, 92% of operating profit) and Engineered Products (18% of revenue, 8% of operating profit). The composite materials segment manufactures and markets carbon fibers, fabrics, specialty reinforcements, prepregs, matrix materials, structural adhesives, and honeycomb that is incorporated into commercial and military aircraft, transportation vehicles, wind turbine blades, recreational products, and other industrial applications. The engineered products segment manufactures and markets composite structures, engineered honeycomb, and RF Interference control primarily for use in the military and aerospace industry.

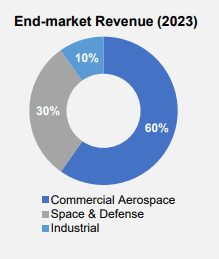

The company operates through three key end-markets, Commercial Aerospace (60% of revenue), Space & Defense (30% of revenue), and Industrial (10% of revenue). The commercial aerospace end-market is the largest user of advanced composites, primarily for manufacturing new commercial aircraft for Boeing and Airbus. The space & defense end market is another user, mainly consisting of military aircraft for the United States and Western European governments. The Industrial end-market includes products for automotive, consumer electronics, wind turbine blades, and other applications. While aerospace and defense end markets carry wide economic moats, the industrial end market is subject to higher levels of competition.

Leading Player in a Secular Growth Market

Hexcel is one of the three major manufacturers of advanced composite materials and holds the #1 position in composite sales and production capacity for the aerospace industry. The other two competitors include Toray (OTCPK:TRYIY), a $7.9 billion Japanese company, and Solvay (OTCPK:SLVYY), a $3.5 billion Belgian chemicals company. Hexcel is the leading composite supplier for Airbus, via its A350 contract, and Toray is the leader for Boeing, via its 777X and 787 contracts. Toray’s most recent data for composite materials segment revenue was ~$1.84 billion, and Solvay’s was approximately ~$1.0 billion. The main differentiator for Hexcel is its RF interference control product (material to keep engines running smoothly) and the production of thermoplastics (used to improve component durability). Moreover, due to the small set of suppliers, Hexcel has a low chance of losing market share.

While barriers to entry for basic carbon fiber production are low, aerospace grade is a different story. Before production, potential entrants must gain access to expensive capital equipment to pass regulatory standards. They then must develop relationships with a small set of raw material providers, and eventually the large OEMs. Even assuming an entrant reaches this point, intellectual property, firm reputation, and new technological developments would be challenging to overcome. Thus, industry disruption should be minimal for the foreseeable future.

Aerospace composite manufacturers are driven by aircraft production volume and the percentage of carbon fiber on each plane, called composite shipsets. Commercial aircraft today consist mostly of aluminum shipsets, but over time advanced composite material will likely take their place. Composite materials are 5x stronger, 30% lighter, and offer lower lifecycle costs than aluminum. New generation widebodies demand the highest amount of composite material per shipset (50%+), and account for ~11% of expected 2025 deliveries. On the other hand, new-generation narrowbodies demand less carbon fiber per shipset (~15%-30%), but account for ~75%+ of expected 2025 deliveries. Per Boeing and Airbus, the breakdown is expected to shift towards widebodies over the next 20 years at ~18% of expected deliveries. This should drive substantially higher sales, as select widebody composite shipsets are $4.5-$5.0 million per aircraft, while narrowbody composite shipsets are only ~$350k per aircraft. To the right, you can see expected delivery levels for Boeing and Airbus, and below you can see composite penetration over time.

Investor Relations

Investor Relations

Significant EPS Growth on Production Ramps

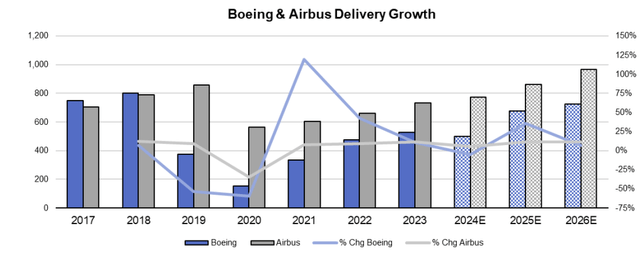

Since 2020, aircraft OEMs have failed to reach delivery goals. Both Boeing and Airbus have faced numerous supplier challenges and continue to push out production expectations. Boeing faces its own challenges from 737 crashes in 2018 and 2019, followed by the door plug blowout in early January. Positively, while aircraft supply remains challenged, demand continues to be robust. Boeing currently has a backlog of ~$515 billion and Airbus has a backlog of ~$554 billion; both near record levels. Below you can see consensus delivery levels across the main commercial programs. Airbus is expected to pass 2018-19 production levels by 2025, and Boeing should see normalization by 2026. Either way, long-term demand should accelerate top-line growth for Hexcel.

Bloomberg

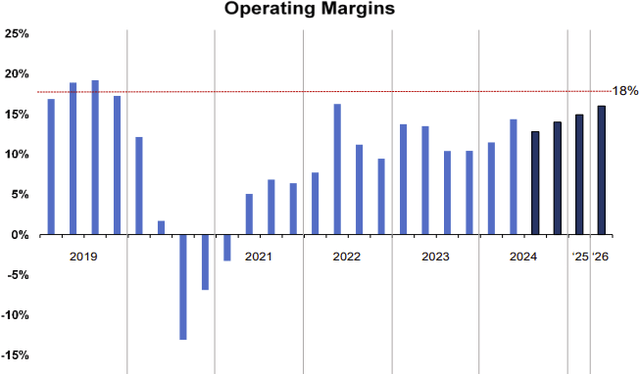

Hexcel’s business model involves cycles of high fixed costs to match OEM delivery expectations. This occurred in 2015–2017 when the firm spent ~15% of sales on capital expenditures annually to match production ramps for 2018 and 2019. While it initially led to strong operating efficiency, by 2021 they experienced a ~13% drop in operating margins as deliveries slowed. Today, HXL is at ~75% capacity utilization vs. 2019, which should easily support production levels over the next three years. Despite this, the street still only has operating margins expanding towards ~16% by 2026, which is below 2019 levels of ~18%. This is also seen in management’s FCF guidance of >$800 million in the next three years, compared to consensus estimates at $778 million. Both these deviations seem unwarranted due to Hexcel’s current cost structure and industry tailwinds. Assuming Hexcel could reach 18% margin and $800 million in three-year cumulative FCF, Hexcel’s stock could see significant upside.

Koyfin

Boeing and Airbus Commentary

In the second quarter of 2024, both Boeing and Airbus faced persistent challenges keeping up with delivery expectations. Boeing’s earnings call highlighted ongoing supply chain disruptions that continue to disrupt production rates across its aircraft portfolio. Despite these challenges, Boeing continues to focus on stabilization, while also enhancing regulatory compliance in relation to increased control standards. The integration of Spirit AeroSystems is also progressing well, and should improve operational efficiency once closed in mid-2025. During the call, Boeing mentioned heightened activity in the defense sector amidst continued geopolitical tensions. They also expect production ramps to improve as deliveries to key markets like China begin to normalize by year-end. Moreover, they officially announced the appointment of Kelly Ortberg as CEO, which investors view as a net positive. Below you can see the announced Boeing production rates

Boeing Production Goals:

737 target of 38 per month at year-end (456 annually) 787 target of 5 per month at year-end (60 annually) 777x first delivery by 2025

During Airbus’s second quarter conference call, management highlighted similar supply chain disruptions, particularly with engines. While this has caused delays for expected deliveries, demand remains robust, with a backlog of ~8,858 aircraft at the end of June. Airbus then highlighted a focus on efficiency, with no restructuring or cost adjustment plans. They expect 770 total deliveries in 2024, and low double-digit percentage annual delivery growth thereafter. Airbus remains optimistic about future growth prospects despite these ongoing operational challenges. Below you can see Airbus’s expected production rates.

Airbus Production Goals:

A320 target of 75 per month by 2027 (900 annually) A350 target of 12 by 2028 (144 annually) 770 total deliveries in 2024 Long-term double-digit delivery growth OEM Delays Create an Attractive Entry Point

While difficult to make a call on when supply chain disruptions will subside, demand isn’t going anywhere. Both Boeing and Airbus are at record backlog levels and expect continued growth over the next 20 years. Hexcel is well positioned with heavy Airbus exposure and should see accelerated growth once supply chains clear up. Boeing, on the other hand, has a longer path to normalization, which most likely won’t occur until 2026 or later. On the supply chain side, both OEMs work with thousands of suppliers, thus trying to forecast stabilization can be difficult. For now, this part of the story involves patience. For Boeing specifically, they are capped at producing 38 737s per month, or 456 per year. This is almost half as many as Airbus and will lead to slower top-line growth for Hexcel. Net/net I believe this uncertainty creates a solid entry point for Hexcel. Once investors see Airbus is on track to reach delivery goals, and Boeing resolves regulatory challenges, Hexcel’s stock should reflect this upside.

Production Today (Q2):

737: ~25 per month 787: ~4 per month A320: ~44 per month A350: ~5 per month Balance Sheet and Cash Flow Analysis

Balance Sheet: Despite Hexcel’s smaller size, the firm has a strong balance sheet with minimal leverage. Hexcel is considered investment grade by Moody’s and Fitch, and is only one level below investment grade for S&P Global. Over the pandemic, they focused on de-levering, bringing its long-term debt down from ~$1.4 billion to ~$800 million today. They now hold a leverage ratio (net debt/EBITDA) of ~2x, with a plan to keep it in the range of 1.5-2.0x. Their outstanding debt at FYE 2023 was entirely fixed rate at ~4.5%.

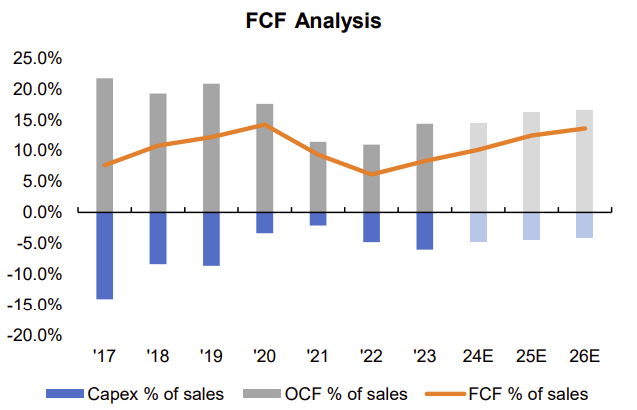

Cash Flow Statement: Hexcel’s cash flow profile is also attractive. Looking below, we see cash flow from operations remained strong in the challenging 2021-2023 environment. We can also see the strength of FCF following its production ramp from 2015-2017, where capex was ~15% of sales three years in a row. Off this, FCF expanded almost ~7% going into 2020, and drove operating cash flow of $491 million in 2019. Moreover, 2018 was the only year they were able to focus on shareholder returns, which drove over $350 million in share buybacks. Moving into 2024-2026, with management expecting minimal capex and M&A activity, Hexcel will most likely return the majority of FCF to shareholders through buybacks.

10-K

Management + Insider Buys

On April 9th, 2024, Hexcel announced the appointment of Thomas Gentile as CEO. Gentile replaces Nick Stanage who has been CEO since 2013 and with Hexcel since 2009. Following the announcement, Hexcel’s stock price dropped ~11%, most likely due to the poor timing of the announcement. It followed the company’s February investor day (first in five years) that provided three-year financial targets, and came before 1Q24 results. Gentile was previously CEO of Spirit AeroSystems, where he faced operational challenges and was abruptly replaced. Positively, Gentile’s experience is likely better suited for Hexcel as 1) Spirit was a major customer of Hexcel, so Gentile should have a good view on customer buying patterns, and 2) Given Spirit’s central role for Boeing (who recently acquired Spirit) and Airbus, he likely understands the direction OEMs are going. Following this announcement, both Gentile and Stanage purchased almost ~$1 million in Hexcel stock, alongside three directors.

OpenInsider

Risks

The key risk for Hexcel is its exposure to Airbus and Boeing. In 2019, Airbus accounted for 39% of revenue and Boeing accounted for 25% (today its ~15%). In this normalized environment, ~64% of revenue was dependent on two key customers. Even if Airbus and Boeing reach expected production levels, this concentration could prove challenging if OEMs face similar issues to that of Boeing in 2018, 2019, and 2024. Additionally, 50% of the thesis relies on production ramps to reach target levels within a certain timeframe. Assuming further delays occur or production numbers are not reached, Hexcel’s price will likely reflect this.

Other sources of risk include Hexcel’s exposure to government contracts. The space and defense end market is responsible for ~30% of revenue and is driven by government spending and geopolitical tensions. While both are high, the upcoming election, potential geopolitical de-escalation, or other global events may hinder results in the near term. The industrials segment, while a small percentage of revenue, has faced negative growth recently. As competition increases and customers search for differentiated suppliers, this segment could face further downside. Additional risks include supplier bottlenecks, lower-than-expected aircraft production growth, and new entrants in aerospace grade composite manufacturing.

Valuation

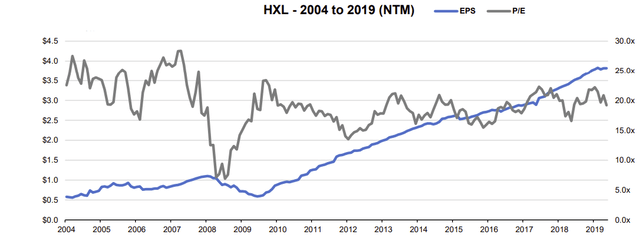

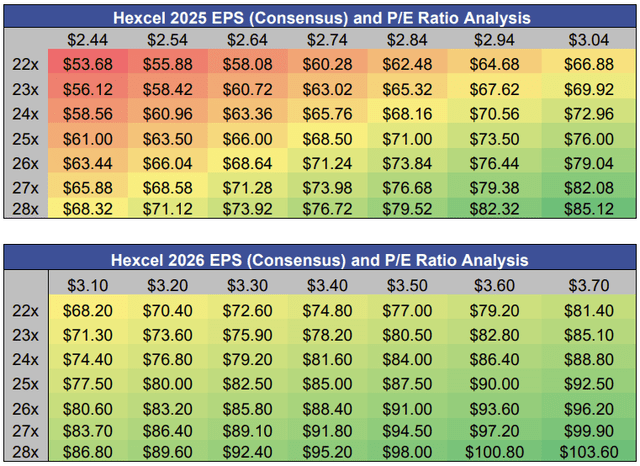

Hexcel benefits from near-term OEM production ramps, and long-term secular growth from composite material adoption. These factors should drive sustainable top-line growth, margin expansion, and share repurchases as capex needs to remain minimal. Hexcel’s valuation assumes trough earnings of $2.37 on NTM basis, and demands a ~25x multiple. With production most likely normalizing in 2026, EPS expectations imply a 27% CAGR over this period. Assuming already in place capacity drives higher-than-expected margins, EPS growth could reach a ~30% CAGR implying $3.55 in EPS by 2026. Keeping the NTM 25x multiple flat would assume an $89 stock price, or 16% annualized upside by 2026. While Hexcel’s historical multiple was around 20x, the composite value proposition should drive less cyclicality, and long-term earnings power. Below, you can see NTM EPS versus P/E ratio.

Bloomberg

Bloomberg

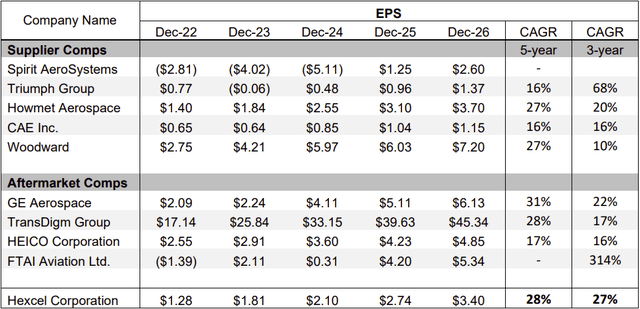

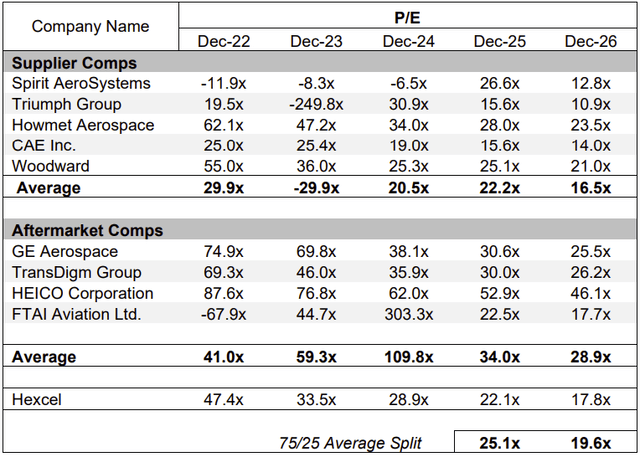

Looking at comps, we note high differentiation in Hexcel’s products compared to other OEM suppliers. The list of comps below was supplied directly by Hexcel’s management, and is broken down by suppliers and aftermarket providers. The first standout seems to be Hexcel’s position above supplier comps but under aftermarket comps in most major areas. This makes sense as Hexcel provides little to no aftermarket services. Some positives to note include Hexcel’s low leverage, above-average EBITDA margin, and robust EPS growth in comparison to peers. This positioning proves positive as comps show a higher than expected multiple based on growth expectations. Looking at both five-year and three-year EPS CAGR, Hexcel is above most peers, excluding Spirit (SPR), Triumph (TGI), and FTAI (FTAI). Positively, these all seem to be outliers as they’ve experienced losses over the last five-years. Despite this, Hexcel is still priced in-line with supplier peers despite outperformance in growth and margins. Using a 75/25 split for suppliers and aftermarket P/E ratios shows a multiple of 25x for 2025, compared to Hexcel’s 22x. Even though Hexcel is differentiated from most peers, this illustrates additional support for an elevated multiple moving forward.

Bloomberg

Author Calculation

Author Calculation

Conclusion

Hexcel’s position as a top manufacturer of aerospace grade composites allows it to stand out against industry peers. With a global presence and leadership in aerospace composite sales, Hexcel’s value is driven by strong customer relationships, success in securing government contracts, and effective cost management. With only 7% of the global commercial aircraft fleet considered composite-rich, there is a significant growth opportunity as fleets shift toward more fuel-efficient, longer-lasting designs. Hexcel’s favorable exposure to Airbus, coupled with its high production capacity, positions it well for future growth. On a near-term basis, supply chain issues prove challenging, but in the long run Hexcel is poised for long-term EPS growth. Even assuming more OEM challenges, the secular theme should prove as a supportive foundation for Hexcel.

Source link : http://www.bing.com/news/apiclick.aspx?ref=FexRss&aid=&tid=66c9bfd2e93745d094abcc2769c06a80&url=https%3A%2F%2Fseekingalpha.com%2Farticle%2F4716881-hexcel-a-secular-and-cyclical-growth-opportunity&c=3445710667598143703&mkt=en-us

Author :

Publish date : 2024-08-23 23:24:00

Copyright for syndicated content belongs to the linked Source.

{kind=link}