Japan has announced a substantial $550 billion package within its trade agreement framework that could facilitate financing for Taiwanese semiconductor manufacturers operating in the United States, Reuters reports. The move underscores Japan’s strategic commitment to bolstering the global semiconductor supply chain amid ongoing geopolitical tensions and supply disruptions. By potentially supporting key Taiwanese chipmakers’ expansion in the U.S., Japan aims to enhance technological collaboration and economic resilience across Asia and North America.

Japan Unveils Major Trade Package Targeting Semiconductor Industry Expansion in the US

Japan has announced an ambitious $550 billion trade initiative aimed at bolstering semiconductor production capabilities in the United States, signaling a strategic push to strengthen supply chains amid global chip shortages. Central to this initiative is a proposed financial framework designed to support Taiwanese chipmakers expanding their manufacturing footprint on American soil. Industry insiders suggest this move will not only solidify Japan’s position within the semiconductor ecosystem but also foster closer economic ties with key US and Taiwanese partners.

The package is expected to offer a range of incentives, including:

Direct funding opportunities for chip fabrication plants

Tax breaks and regulatory support for foreign investors

Public-private partnerships facilitating innovation and workforce development

Component

Estimated Value

Impact Area

Manufacturing Grants

$250B

US-based Fab Construction

R&D Investments

$150B

Innovation & Tech Development

Workforce Training

$100B

Skilled Labor Programs

International Collaboration

$50B

Cross-border Partnerships

Implications for Taiwan’s Chipmakers Amid Increasing Global Tech Competition

Taiwanese chipmakers stand at a critical crossroads as global tech giants ramp up competition amidst shifting geopolitical landscapes. The announcement of Japan’s $550 billion financing package as part of its new trade deal could serve as a strategic springboard for Taiwan’s semiconductor industry to expand operations in the United States. This infusion of capital aims to fuel domestic manufacturing capabilities, supporting chipmakers in circumventing supply chain disruptions and regulatory uncertainties while bolstering innovation capacity outside Asia.

Key implications for Taiwan’s chip manufacturers include:

Enhanced US Presence: Access to funding lowers barriers for establishing new fabrication plants on American soil, diversifying production bases.

Technology Collaboration: Increased investment opens doors for joint ventures, accelerating cutting-edge research in AI chips and 5G components.

Supply Chain Security: Strengthened resilience against geopolitical tensions that have recently threatened raw material access and logistics.

Competitive Edge: By leveraging international financial support, Taiwanese firms can better compete with other global chipmakers, especially given rising manufacturing costs in Asia.

Focus Area

Potential Benefit

Manufacturing Expansion

Local factories reduce dependency on Asia

R&D Investment

Faster innovation cycles, new chip designs

Geopolitical Risk Mitigation

Reduced impact from trade tensions

Market Diversification

New customer bases, stronger global footprint

Policy Recommendations for Strengthening US-Japan-Taiwan Semiconductor Collaboration

To bolster the semiconductor supply chain amid rising geopolitical tensions, the three governments should prioritize targeted investments that leverage the strengths of each party. Strategic funding initiatives can create a robust ecosystem where Taiwanese chipmakers benefit from Japan’s advanced manufacturing technologies and the US’s vast consumer market. Facilitating public-private partnerships, especially under the ambitious $550 billion trade framework, will be critical to nurturing innovation hubs in key regions across the US and Japan. Such collaborative efforts would significantly reduce supply chain vulnerabilities and promote technology sharing that propels the entire industry forward.

Policy frameworks should also focus on enhancing regulatory alignment and intellectual property protections to ensure smooth cross-border operations. Some recommended steps include:

Streamlining export controls to prevent bottlenecks in chip component shipments.

Implementing tax incentives for joint R&D projects between Japanese and Taiwanese firms operating in the US.

Establishing a trilateral cybersecurity protocol to safeguard semiconductor manufacturing data.

As negotiations continue to shape the future of semiconductor manufacturing and international trade, Japan’s potential $550 billion contribution underscores the high stakes involved in securing technological leadership and supply chain resilience. The proposed financing for a Taiwanese chipmaker’s U.S. operations highlights the strategic importance countries place on advanced chip production amid global geopolitical tensions. Stakeholders and observers alike will be closely watching how this large-scale collaboration unfolds and what it means for the broader tech industry and economic alliances moving forward.

Saudi Arabia’s parcel delivery sector has marked a significant milestone in the second quarter of 2025, with over 50 million parcels successfully delivered across the kingdom, according to data analyzed on TradingView. This surge underscores the rapid expansion of e-commerce and logistics infrastructure within the country, reflecting shifting consumer behaviors and growing demand for efficient last-mile delivery services. Industry experts suggest that this trend not only highlights the robustness of Saudi Arabia’s supply chain capabilities but also points to broader economic implications as the nation advances its Vision 2030 goals.

SNG Achieves Significant Milestone in Saudi Parcel Deliveries Reflecting Robust E-commerce Growth

SNG’s delivery network has demonstrated unparalleled efficiency by surpassing the 50 million parcel mark in the second quarter of 2025, setting a new benchmark within the Saudi Arabian logistics sector. This milestone not only highlights the company’s operational prowess but also mirrors the accelerated adoption of digital retail channels across the region. SNG’s strategic investments in automation and last-mile delivery innovations have played a critical role in managing this unprecedented surge, ensuring timely and accurate dispatches even during peak demand periods.

The sustained growth in parcel volume reflects broader trends reshaping the e-commerce ecosystem in Saudi Arabia. Key factors contributing to this uptrend include:

Expansion of diverse product categories favored by consumers

Government initiatives encouraging digital infrastructure development

Metric

Q2 2024

Q2 2025

Growth %

Parcels Delivered

38M

50M+

31.6%

Delivery Speed (avg hrs)

36

28

-22.2%

Customer Satisfaction

88%

93%

+5%

Key Drivers Behind Rapid Expansion in Saudi Logistics Sector

Government initiatives such as the Saudi Vision 2030 have been instrumental in transforming the logistics landscape. Massive investments in infrastructure, including the expansion of ports like Jeddah and Dammam, and the development of modern industrial zones, have enhanced connectivity and efficiency. This strategic push supports not only domestic trade but also establishes Saudi Arabia as a crucial global logistics hub bridging Asia, Europe, and Africa.

Technological advancements have further accelerated growth, with companies adopting state-of-the-art supply chain management systems and leveraging data analytics to optimize delivery routes and enhance customer experiences. The boom in e-commerce, fueled by a digitally savvy population, is driving parcel volumes to unprecedented levels. Key factors include:

Integration of AI-driven logistics solutions to reduce delivery times

Expansion of last-mile delivery networks to underserved regions

Strong partnerships between public and private sectors

Driver

Impact

2025 Projection

Infrastructure Investment

Enhanced capacity & network reach

25% increase in cargo throughput

Digital Transformation

Improved efficiency & customer satisfaction

35% faster delivery times

E-commerce Growth

Surge in parcel volumes

Delivery of 50+ million parcels in Q2

Strategic Recommendations for Sustaining Delivery Efficiency and Market Competitiveness

To maintain its impressive delivery efficiency amid rising parcel volumes, SNG should prioritize the integration of advanced logistics technologies. Implementing AI-driven route optimization and real-time tracking systems can significantly reduce transit times and operational costs. Embracing automation in warehousing and last-mile delivery-with innovations like drone-assisted drops or autonomous vehicles-will position SNG as a forward-thinking leader, adapting swiftly to evolving customer expectations in the Saudi Arabian market.

Key strategic actions include:

Investing in scalable IT infrastructure for dynamic demand forecasting

Enhancing partnerships with local and international couriers to expand reach

Prioritizing sustainable delivery practices to align with regional environmental goals

Developing customer-centric platforms to increase transparency and user engagement

Strategy

Impact

Timeline

AI-based route optimization

15% faster deliveries

Q3 2025

Automated warehousing

20% cost reduction

Q4 2025

Green delivery initiatives

Improved brand reputation

2026 onwards

Final Thoughts

As SNG surpasses the milestone of delivering over 50 million parcels in Saudi Arabia during the second quarter of 2025, the company solidifies its position as a key player in the region’s rapidly expanding e-commerce and logistics sectors. This achievement underscores not only SNG’s operational efficiency but also the growing demand for fast and reliable delivery services across the Kingdom. Market watchers will be keen to see how SNG leverages this momentum moving forward, especially as digital commerce continues to reshape consumer behavior in Saudi Arabia and beyond.

China’s dominance in rare earth mineral production has shaped global technology and manufacturing industries for decades. However, behind the high-tech gadgets and clean energy solutions lies a complex and often troubling story. NPR’s latest investigation delves into the downstream environmental, economic, and geopolitical impacts of China’s rare earth mining practices. From ecological degradation and toxic pollution to shifts in international supply chains, the report sheds light on how these critical materials are influencing the world far beyond the mine sites.

China’s Rare Earth Mining Impact on Global Supply Chains

China’s dominance in rare earth mining reverberates throughout global manufacturing, shaping the technological and industrial sectors worldwide. Controlling approximately 60% of global rare earth processing, the country’s mining policies directly influence everything from smartphone production to electric vehicle supply chains. Disruptions or policy shifts in China have sparked volatility in global markets, forcing multinational companies to reassess their sourcing strategies and supply chain resilience.

Several key impacts can be observed:

Price Volatility: Fluctuating rare earth availability drives unpredictable costs for electronics and clean energy components.

Supply Chain Bottlenecks: Dependence on Chinese export quotas delays manufacturing timelines internationally.

Geopolitical Risks: Trade tensions amplify concerns over raw material accessibility.

Country

Rare Earth Production Share (%)

Key Industries Affected

China

60%

Electronics, EVs, Defense

United States

15%

Aerospace, Renewable Energy

Australia

12%

Mining, Battery Production

The section you provided offers a clear overview of China’s pivotal role in rare earth mining and its global implications. Here’s a summary and a few considerations if you want to enhance or present the content:

Summary:

China controls around 60% of global rare earth processing, heavily impacting worldwide manufacturing, especially in electronics, electric vehicles, and defense.

Key impacts include price volatility, supply chain bottlenecks, and geopolitical risks.

The table shows production shares for China (60%), the United States (15%), and Australia (12%) along with the key industries each supports.

Suggestions:

Complete the Table: The provided table snippet cuts off after Australia. Commonly, other countries like Russia, India, and some African nations also contribute. Including them could give a fuller picture.

Add Visuals or Graphs: A pie chart illustrating production shares would quickly convey China’s dominance.

Clarify Source or Data Year: Adding a reference or the year of data enhances credibility.

Explain Rare Earths: For readers unfamiliar, a brief explanation of what rare earth elements are and why they matter could contextualize the importance.

Supply Chain Strategies: Expand on how companies are adapting-e.g., investing in recycling, developing alternative materials, or diversifying mines.

If you want, I can help create or expand on any part!

Environmental Consequences of Extraction Practices in Inner Mongolia

“`html

The intense mining activities in Inner Mongolia, a global hub for rare earth elements, have triggered significant environmental degradation. Open-pit extraction has resulted in landscape scarring and soil erosion, severely disrupting local ecosystems. The widespread use of hazardous chemicals in processing rare earth ores contaminates water sources, leading to alarming levels of heavy metals in rivers and groundwater. These pollutants not only harm aquatic life but also pose serious health risks to nearby communities relying on these water supplies for agriculture and daily use.

Moreover, the release of toxic waste has led to deforestation and loss of biodiversity, threatening endemic plant and animal species. The following table highlights the key environmental impacts observed in the region:

Impact

Affected Area

Severity

Soil contamination

500+ km²

High

Water pollution

Thousands of km of rivers

Severe

Loss of biodiversity

Critical habitats

Significant

Acid mine drainage has lowered pH levels in surrounding rivers.

Airborne dust from excavation sites contributes to respiratory issues.

Deforestation undermines carbon sequestration efforts It looks like your last list item is incomplete. Here’s the corrected and completed version of your HTML snippet for the list and the entire block:

“`html

The intense mining activities in Inner Mongolia, a global hub for rare earth elements, have triggered significant environmental degradation. Open-pit extraction has resulted in landscape scarring and soil erosion, severely disrupting local ecosystems. The widespread use of hazardous chemicals in processing rare earth ores contaminates water sources, leading to alarming levels of heavy metals in rivers and groundwater. These pollutants not only harm aquatic life but also pose serious health risks to nearby communities relying on these water supplies for agriculture and daily use.

Moreover, the release of toxic waste has led to deforestation and loss of biodiversity, threatening endemic plant and animal species. The following table highlights the key environmental impacts observed in the region:

Impact

Affected Area

Severity

Soil contamination

500+ km²

High

Water pollution

Thousands of km of rivers

Severe

Loss of biodiversity

Critical habitats

Significant

Acid mine drainage has lowered pH levels in surrounding rivers.

Airborne dustPolicy Recommendations to Mitigate Economic and Ecological Risks

To address the multifaceted challenges arising from rare earth mining in China, policy frameworks must balance economic growth with ecological preservation. Governments and international bodies can implement stricter environmental regulations that mandate cutting-edge, sustainable mining technologies and enforce penalties for illegal or harmful extraction practices. Encouraging transparency through mandatory reporting and independent audits will further ensure compliance and foster public trust.

Promote diversification in global rare earth supply chains to reduce reliance on a single source

Invest in research for recycling and alternative materials to alleviate mining pressures

Support local communities affected by mining through compensation and sustainable development programs

Enhance international cooperation to create unified standards and share best practices

Economic incentives can be leveraged to revolutionize current practices: subsidies for green mining techniques, tax credits for companies investing in circular economy models, and funding for technological innovation represent pivotal strategies. Below is a concise overview of recommended policy instruments and their expected impact on both economy and ecology.

As global demand for rare earth elements continues to surge, the downstream effects of China’s mining practices underscore a complex web of environmental, economic, and geopolitical challenges. NPR’s exploration sheds light on how these critical materials, essential to modern technology, come with significant costs that reverberate far beyond the mines themselves. Understanding this dynamic is crucial for policymakers, industries, and consumers alike as they navigate a future increasingly dependent on these indispensable resources.

Malaysia has announced stricter regulations on the movement of U.S.-made artificial intelligence (AI) chips within its borders, a move poised to impact the global semiconductor supply chain. The new rules, detailed in a recent Wall Street Journal report, come amid escalating geopolitical tensions and increasing scrutiny over advanced technology exports. As Malaysia plays a critical role in the manufacturing and distribution of AI hardware, these tighter controls signal a significant shift in the country’s trade and security policies related to cutting-edge technology.

Malaysia Imposes Stricter Controls on Export of U.S.-Manufactured AI Chips

In a move reflecting growing geopolitical concerns, Malaysian authorities have introduced heightened regulations governing the export and transit of artificial intelligence (AI) chips manufactured in the United States. The new rules specifically target semiconductors critical to AI development, demanding stringent documentation, export licenses, and prior approvals from relevant government bodies. This tightening of controls aims to prevent sensitive technologies from being routed through Malaysia to nations under U.S. export restrictions, signaling Kuala Lumpur’s alignment with broader international efforts to manage the proliferation of advanced AI components.

Key highlights of the updated export framework include:

Mandatory Licensing: Exporters must obtain explicit permits for all shipments containing U.S.-origin AI chips.

Enhanced Screening: Increased scrutiny at border checkpoints to track and verify shipment contents more accurately.

Penalties for Non-Compliance: Heavy fines and possible export bans for entities failing to adhere to the restrictions.

Control Aspect

Previous Policy

New Regulation

Export Documentation

Standard customs declaration

Detailed export license and origin certification required

Targeted Technologies

Broad semiconductor category

Specific focus on AI-enabled chips made in the U.S.

Enforcement

Random inspections

Systematic shipments screening and tracking

Implications for Global Tech Supply Chains and Regional Security Dynamics

Malaysia’s heightened restrictions on the export and transit of U.S.-manufactured AI chips signal a strategic recalibration with far-reaching consequences. This move disrupts established supply chains, especially those involving semiconductor components vital to advanced technologies. Industry stakeholders now face increased scrutiny, longer lead times, and potential rerouting of shipments through alternative countries, amplifying logistical costs and operational uncertainty.

Increased complexity in compliance as companies navigate Malaysia’s regulatory environment alongside U.S. export controls.

Potential delays in the delivery of critical AI components, impacting production timelines for tech firms worldwide.

Heightened risk for multinational firms sourcing chips passing through Southeast Asia, prompting diversification of manufacturing sites.

On the geopolitical front, Malaysia’s policy adjustment underscores the intricate dynamics shaping regional security. The country’s decision reflects a balancing act between maintaining strong economic ties with the U.S. and managing its relationships with neighboring powers amidst escalating U.S.-China technology competition. Analysts suggest this may lead to a recalibration of defense postures and alliances in the Indo-Pacific region, where technological assets increasingly intersect with national security interests.

Aspect

Impact

Regional Implication

Tech Exports

Raised Barriers

Slower Cross-Border Trade

Supply Chain

Increased Complexity

Supply Diversification

Security

Heightened Caution

Shift in Alliances

Recommendations for Companies Navigating New Regulatory Landscape in Malaysia

Companies operating within Malaysia’s tech and manufacturing sectors must adopt a proactive approach to compliance amid evolving restrictions on the export and distribution of U.S.-made AI chips. Establishing a dedicated regulatory monitoring team is crucial for staying ahead of frequent updates and interpreting the nuanced guidelines imposed by both Malaysian authorities and international partners. Additionally, firms should prioritize transparency in supply chain operations-from sourcing to final delivery-to mitigate risks of inadvertent violations. This includes rigorous documentation and real-time tracking systems that align with governmental reporting requirements.

Engagement with local legal experts and industry associations can facilitate a clearer understanding of compliance mandates and foster collaborative advocacy. Companies are also encouraged to implement comprehensive internal training programs for teams involved in logistics, procurement, and export controls. The table below outlines key areas of focus for companies adapting to the new regulatory framework:

Regular workshops on export controls and reporting

Insights and Conclusions

As Malaysia enforces stricter controls on the movement of U.S.-made AI chips, the move underscores the growing geopolitical complexities surrounding advanced semiconductor technologies. Industry stakeholders and policymakers alike will be watching closely to assess the broader implications for global supply chains and technological innovation. The evolving regulatory landscape signals a cautious approach amid heightened scrutiny of critical hardware, portending further shifts in the intersection of technology and international relations.

In the remote landscapes of northern Myanmar, the extraction of rare earth minerals has emerged as a critical yet contentious industry, fueling both economic opportunities and ongoing conflicts. According to a recent report by the Stimson Center, the burgeoning rare earth mining sector is deeply intertwined with local armed groups and complex political dynamics, raising serious concerns about governance, human rights, and regional stability. This article delves into how the demand for these strategic minerals is shaping conflict economies in the area and what it means for Myanmar’s future amid broader geopolitical interests.

Rare Earth Mining Drives Economic Gains and Fuels Armed Conflict in Northern Myanmar

In the rugged landscapes of northern Myanmar, the extraction of rare earth elements has rapidly transformed into a critical economic driver. Communities have experienced a surge in local employment and infrastructure development, fueled by the global demand for these minerals essential to modern technologies. However, this prosperity is shadowed by the intricate networks of armed groups capitalizing on mining revenues to sustain their operations. These groups exert control over lucrative sites, leveraging mineral wealth to procure arms and maintain territorial dominance.

The consequences extend beyond mere economic shifts, as the overlap between mining interests and conflict has intensified local instability. Multiple factions vie for influence over mining zones, resulting in sporadic clashes that jeopardize civilian safety and disrupt production. The dynamics underlying this nexus are captured in the table below:

Aspect

Details

Primary Minerals

Neodymium, Dysprosium, Terbium

Major Stakeholders

Ethnic Armed Organizations, Local Militias, Private Mining Firms

Regional instability exacerbated by competing mining interests.

Governance challenges hinder regulation and sustainable development.

International demand ensures continued pressure on resource extraction.

Environmental and Social Impacts of Unregulated Mining Operations on Local Communities

In northern Myanmar, the surge of unregulated rare earth mining has left local communities grappling with severe environmental degradation and social unrest. Toxic chemicals released during mining contaminate soil and waterways, disrupting livelihoods dependent on agriculture and fishing. Forests are cleared without regard for biodiversity, accelerating habitat loss and threatening endangered species. Moreover, the lack of formal oversight means that waste disposal practices are often unsafe, exacerbating water pollution and health risks for nearby villages.

The social fabric of these regions also unravels under the weight of mining activities. Displacement and land disputes have intensified, as miners encroach on indigenous territories without consent or fair compensation. Often operating outside state control, these mines become hotbeds for armed groups and illicit networks, fueling violence and undermining local governance. Key impacts include:

Health crises: Respiratory and waterborne diseases linked to pollution

Child labor: Exploitative work conditions in dangerous mining sites

Economic instability: Reliance on volatile mining revenues destabilizes communities

Impact Area

Description

Community Effect

Environmental

Soil and water contamination

Crop failures; contaminated drinking water

Social

Forced displacement

Loss of ancestral lands; cultural erosion

Health

Exposure to toxic substances

Increased illness and mortality rates

Security

Presence of armed groups

Conflict escalation; reduced safety

Policy Recommendations for Sustainable Resource Governance and Conflict Reduction

To address the complex challenges posed by rare earth mining in Northern Myanmar, a multi-stakeholder approach is essential. This includes empowering local communities through transparent resource management frameworks, ensuring their active participation in decision-making processes. Strengthening legal frameworks that regulate mining operations will reduce illicit activities and limit the influence of armed groups who exploit the resource economy. Additionally, implementing rigorous environmental assessments and monitoring can mitigate ecological damage while fostering sustainable economic benefits for the region.

International cooperation and targeted development aid must be aligned with conflict-sensitive strategies. This involves coordinating efforts between governments, NGOs, and private sectors to channel investments into social infrastructure and alternative livelihoods, reducing communities’ dependence on conflict economies. The following priorities should guide policy actions:

Enhance transparency via blockchain-enabled supply chain tracking

Implement conflict-sensitive mineral certification schemes

Support capacity-building programs for local law enforcement

Foster cross-border dialogue to manage shared mineral resources

Policy Focus

Expected Outcome

Key Stakeholders

Transparent Licensing

Reduce illegal mining

Government, Local Authorities

Community Engagement

Empower locals, build trust

Communities, NGOs

Environmental Safeguards

Protect ecosystems

Environmental Agencies

Conflict-Sensitive Aid

Decrease armed group influence

International Partners

Concluding Remarks

As Northern Myanmar continues to be a focal point for rare earth mining, the intersection of valuable resources and ongoing conflict presents a complex challenge for regional stability and global supply chains. Addressing the humanitarian and environmental impacts alongside economic interests remains critical. The Stimson Center’s insights underscore the urgent need for transparent governance and international cooperation to navigate the intricate landscape of rare earth extraction in this volatile region. Without concerted efforts, the cycle of conflict and exploitation tied to these essential minerals is likely to persist, with far-reaching consequences beyond Myanmar’s borders.

In a surprising development that could reshape global tech manufacturing dynamics, reports have emerged of the Chinese government reportedly instructing Foxconn engineers to “leave India,” raising fresh questions about Apple’s manufacturing strategies. As Foxconn plays a pivotal role in assembling Apple’s flagship devices, this directive signals potential disruptions in the company’s efforts to diversify production beyond China. Industry insiders and analysts are now closely scrutinizing what this move might mean for Apple’s ambitious plans to expand its footprint in India, a market touted as a critical growth frontier for the tech giant.

Chinese Government’s Directive to Foxconn Engineers Signals Shifting Dynamics in Apple’s Manufacturing Strategy

The recent directive from Chinese authorities instructing Foxconn engineers to exit India underscores a significant recalibration in Apple’s global manufacturing blueprint. This move hints at Beijing’s intensified efforts to consolidate production within China, potentially complicating Apple’s ongoing diversification strategy aimed at reducing reliance on a single hub. The instruction not only impacts Foxconn’s operational agility but also highlights the broader geopolitical tensions influencing supply chain decisions and international trade policies.

Industry analysts suggest that this development could accelerate Apple’s pivot towards alternative manufacturing locations such as Vietnam and Indonesia, as well as prompt a re-evaluation of investment priorities. The unfolding scenario is expected to affect:

Supply chain resilience: Balancing geopolitical risks with production efficiency.

Cost considerations: Potential shifts in labor and logistics expenses across regions.

Market access: Navigating regulatory environments and trade agreements outside China and India.

Country

Manufacturing Strengths

Potential Challenges

China

Robust infrastructure, Skilled workforce

Geopolitical tensions, Regulatory control

India

Growing market, Cost-effective labor

Regulatory hurdles, Recent governmental friction

Vietnam

Rising manufacturing hub, Favorable trade deals

Infrastructure gaps, Workforce skill development

Implications for Apple’s Supply Chain Amid Rising Geopolitical Tensions Between China and India

Apple’s intricate supply chain, long reliant on the synergy between Chinese manufacturing hubs and expanding Indian facilities, now faces an unexpected crossroads. The Chinese government’s recent directive instructing Foxconn engineers to distance themselves from operations in India accentuates geopolitical undercurrents shaping global tech production. This move may disrupt the delicate balance Apple has been cultivating to diversify its assembly lines outside China amidst growing calls for supply chain resilience.

Key consequences for Apple’s supply chain include:

Delays in scaling Indian production: Reduced on-ground technical expertise could hinder ramp-up efforts at Foxconn’s Indian plants.

Heightened cost pressures: Relocating specialized personnel or finding alternative engineering resources may increase operational expenses.

Strategic recalibration: Apple might accelerate investments in other Southeast Asian countries or revisit partnerships within China to mitigate risks.

Region

Current Role

Potential Impact

China

Manufacturing & R&D Hub

Stricter export of engineering personnel; production focus

Increased investment and accelerated capacity building

As Apple navigates these shifting geopolitical dynamics, stakeholders should monitor developments closely. The company’s ability to swiftly adapt its global footprint will be crucial in maintaining supply chain robustness and meeting escalating consumer demand worldwide.

If you want, I can help you draft additional analysis or alternative versions!

Strategic Recommendations for Apple to Mitigate Risks and Diversify Production Beyond China and India

In light of recent geopolitical tensions underscored by the Chinese government’s directive to Foxconn engineers to reduce involvement in India, Apple faces a critical juncture in its supply chain strategy. To safeguard against disruptions and regulatory hurdles, the company must accelerate diversification efforts beyond its heavy reliance on China and emerging operations in India. This includes exploring alternative manufacturing hubs in Southeast Asia, such as Vietnam, Indonesia, and Malaysia, which offer competitive labor costs and growing industrial infrastructure. Furthermore, Apple should deepen partnerships with local suppliers in these regions to nurture resilient ecosystems capable of adapting swiftly to geopolitical shifts.

To effectively manage this transition, Apple can implement a multi-pronged approach focusing on flexibility and risk mitigation:

Invest in automation and smart manufacturing technologies to reduce dependency on specific geographic labor pools.

Establish regional manufacturing clusters that can share production loads in case of localized disruptions.

Enhance supply chain transparency and agility through advanced data analytics and real-time monitoring systems.

Region

Key Advantage

Risk Level

Vietnam

Cost-effective manufacturing

Moderate

Indonesia

Growing industrial base

Low to moderate

Mexico

Region

Key Advantage

Risk Level

Vietnam

Cost-effective manufacturing

Moderate

Indonesia

Growing industrial base

Low to moderate

Mexico

Proximity to US market and trade agreements

Low

Let me know if you want me to help you expand on this content, improve styling, or anything else!

In Conclusion

As tensions between China and India continue to shape the geopolitical landscape, the Chinese government’s directive for Foxconn engineers to leave India underscores the complexities facing multinational corporations like Apple. This development not only highlights the fragile nature of cross-border manufacturing partnerships but also signals potential challenges ahead for Apple’s ambitions to diversify its supply chain outside China. As the situation evolves, industry watchers and stakeholders will be closely monitoring how this directive influences Apple’s production strategy and the broader tech manufacturing ecosystem in the region.

China is poised to become the world’s leading semiconductor foundry hub by 2030, according to industry analysis highlighted by Tom’s Hardware. Despite ongoing U.S. export restrictions aimed at curbing Beijing’s technological ambitions, China is on track to command roughly 30% of the global installed semiconductor manufacturing capacity, potentially overtaking Taiwan’s longstanding dominance in the sector. This shift underscores the accelerating efforts within China to bolster its domestic chip production capabilities amid geopolitical tensions and supply chain realignments reshaping the global semiconductor landscape.

China’s Strategic Investments Fuel Rapid Growth in Semiconductor Foundry Capacity

China’s aggressive push into semiconductor foundry capacity is reshaping the global chip manufacturing landscape. Despite ongoing US export restrictions and strict technology controls designed to slow Beijing’s momentum, the nation’s strategic investments in state-of-the-art fabs and local supply chains show no signs of abating. Chinese foundries are rapidly scaling up, driven by vast government subsidies, advanced research initiatives, and partnerships with domestic tech giants aiming to reduce dependency on foreign technology. This robust ecosystem enables China to capitalize on emerging opportunities in 5G, automotive semiconductors, and IoT sectors, positioning itself as a future leader in chip production.

Analysts project that by 2030, China will command approximately 30% of the world’s installed foundry capacity, surpassing Taiwan’s current dominance. Key contributing factors include:

Expansive fab construction: An increasing number of large-scale fabrication plants supporting advanced nodes.

Analyzing the Impact of US Export Controls on China’s Semiconductor Ambitions

The persistent US export controls targeting China’s semiconductor industry, designed to slow the nation’s ascent in chip manufacturing, appear to have only reshaped the landscape rather than halted progress. Despite stringent restrictions on advanced lithography equipment and design software, China is aggressively expanding its domestic foundry capabilities, leveraging government subsidies, strategic partnerships, and indigenous innovation to bridge technological gaps. This multifaceted approach enables Chinese firms to focus on mature and mid-range process nodes, where global demand remains robust, ensuring steady growth in manufacturing capacity.

Key factors driving China’s resilience include:

Massive state-backed investments: Enhanced funding fuels research & development and infrastructure projects.

Talent cultivation: Increased focus on semiconductor education and training programs to build a skilled workforce.

Supply chain localization: Reducing dependencies abroad by cultivating domestic suppliers for raw materials and equipment.

International collaborations: Selective partnerships with non-US entities to access alternate technology avenues.

Metric

2023

Projected 2030

Change (%)

China’s Installed Capacity

18%

30%

+67%

Taiwan’s Installed Capacity

25%

28%

+12%

Global Market Share

100%

100%

–

While the US controls limit access to the latest extreme ultraviolet (EUV) lithography tools, China’s strategic pivot towards incrementally improving mature technologies and amplifying volume production is set to reshape the semiconductor foundry market dynamically. Whether this growth translates into long-term technological leadership remains to be seen, but the expanding footprint signals a competitive global semiconductor ecosystem that is increasingly multipolar.

Recommendations for Global Stakeholders to Navigate the Evolving Semiconductor Landscape

As China is poised to command nearly a third of the global semiconductor foundry capacity by 2030, international stakeholders must rethink strategic alliances and investment priorities. Collaboration with Chinese fabs could unlock access to expansive market opportunities despite ongoing US restrictions. At the same time, diversifying supply chains by strengthening partnerships beyond Taiwan and South Korea will be critical to mitigate geopolitical risks and ensure resilience against potential disruptions.

To thrive in this evolving landscape, global players should consider adopting multifaceted approaches:

Invest in emerging semiconductor hubs in Southeast Asia and Europe to balance the concentration of manufacturing power.

Enhance R&D cooperation focused on next-generation chip architectures and advanced materials to maintain technological leadership.

Monitor policy shifts closely to capitalize on incentives and navigate export controls effectively.

Promote workforce skill development globally to address labor shortages and support innovative production techniques.

Stakeholder

Key Action

Expected Outcome

Chip Designers

Expand foundry partnerships beyond US and Taiwan

Reduced supply bottlenecks

Investors

Target emerging markets and tech startups

Diversified portfolios and growth potential

Policymakers

Craft balanced trade and export policies

Stable international cooperation

In Summary

As China continues to invest heavily in its semiconductor manufacturing capabilities, industry analysts predict that by 2030, the nation could command as much as 30% of the global installed foundry capacity-surpassing longtime leader Taiwan. This ambitious growth trajectory comes despite ongoing U.S. restrictions aimed at curbing China’s technological advancements. The evolving landscape underscores a shifting balance of power in the semiconductor sector, with significant implications for global supply chains and geopolitical dynamics in the years ahead.

As the U.S.-China trade war escalated under the Trump administration, American ports found themselves on the front lines of a sweeping economic battle. Tariffs imposed on a range of imported goods created ripple effects that disrupted supply chains and strained logistics hubs across the country. This article examines how key U.S. ports bore the brunt of tariff-induced slowdowns, highlighting the challenges faced by workers, businesses, and local economies caught in the crossfire of escalating trade tensions.

Impact of Trump’s Tariffs on Key U S Ports Operational Challenges and Delays

Throughout the implementation of the tariffs, major U.S. ports such as Los Angeles, Seattle, and Houston grappled with a surge in operational complexities that strained their established logistics frameworks. Cargo backlogs became commonplace as importers and exporters adjusted to new tax burdens and shifting supply chains. These disruptions led to intensified competition for limited dock space and trucking resources, further magnifying delays in freight clearance and distribution. Port authorities reported bottlenecks not only at entry points but also across inland transit corridors, where heightened inspection protocols compounded congestion issues.

The ripple effects extended beyond scheduling delays, noticeably impacting labor allocation and cost structures within port operations. To illustrate the shift in throughput before and after tariff imposition, below is a summary comparing average monthly container volumes (in TEUs) at selected ports:

Port

Pre-Tariff Avg. Monthly Volume

Post-Tariff Avg. Monthly Volume

Volume Change

Los Angeles

750,000 TEUs

620,000 TEUs

-17.3%

Seattle

210,000 TEUs

180,000 TEUs

-14.3%

Here is a continuation and completion of the table in your HTML section, along with a concluding paragraph to wrap up the analysis:

Houston

130,000 TEUs

115,000 TEUs

-11.5%

The data highlights a significant decline in container volumes across all three ports post-tariff, reflecting the broad impact of increased trade barriers on maritime freight activity. Such volume reductions have led to intensified operational strain as ports attempt to adapt to fluctuating cargo demands while managing persistent logistical challenges. Moving forward, strategic investments in infrastructure and technology will be essential for these ports to enhance throughput efficiency and mitigate the ongoing effects of tariff-induced disruptions.

Would you like me to help with any further edits or additions?

Economic Strain on Local Businesses and Supply Chains at Affected Ports

Local businesses situated near key U.S. ports have been grappling with unprecedented cost increases and logistical challenges following the imposition of tariffs. These surcharges disrupted established supply chains, forcing many companies to either absorb higher import expenses or pass them along to consumers. Small and medium-sized enterprises, in particular, found themselves disproportionately burdened, with many reporting delays in receiving critical inventory and raw materials. The ripple effect has strained margins and, in some cases, led to workforce reductions and deferred investments.

Supply chain volatility manifested in several critical ways, including:

Increased shipping times due to re-routing and congested ports

Rising handling fees impacting profitability

Inventory shortages disrupting production schedules

Shifts in supplier relationships as businesses sought tariff-free alternatives

Port

Impact on Local Biz

Supply Chain Disruption

Port of Los Angeles

Revenue down 15%

3-week delays in container unloading

Port of Seattle

Inventory backlogs increased 25%

Rerouted shipments from Asia

Port of Charleston

Worker layoffs – 8%

Customs inspections slowed clearance

Strategies for Ports to Adapt and Mitigate Future Trade Policy Risks

In an era marked by volatility in global trade, U.S. ports are increasingly prioritizing diversification of trade partners and investment in resilient infrastructure. By expanding access to alternative markets in Asia, Europe, and Latin America, ports can soften the blows from sudden tariff hikes or policy shifts. Enhanced digitalization, including real-time cargo tracking and automated customs clearance systems, is proving critical in minimizing delays and reducing operational costs, thereby helping ports sustain competitiveness amid fluctuating trade landscapes.

Strategic collaboration between port authorities, freight companies, and government agencies also emerges as a cornerstone for mitigating risks. Key adaptive measures include:

Developing flexible supply chains that can quickly pivot in response to new trade measures.

Investing in infrastructure upgrades to accommodate larger vessels and diversified cargo types.

Advancing workforce training to manage emerging logistics technologies and compliance regulations efficiently.

Strategy

Benefit

Example Port

Diversified Trade Routes

Reduces dependency on single markets

Port of Savannah

Digital Infrastructure

Speeds customs processing

Port of Los Angeles

Collaborative Partnerships

Improves adaptability to policy changes

Port of New York & New Jersey

The Way Forward

As the trade war intensified under the Trump administration, U.S. ports found themselves at the frontline of economic disruption. The tariffs reshaped shipping patterns, strained infrastructure, and challenged the resilience of local economies dependent on global trade. Moving forward, the experiences of these ports underscore the complex ripple effects of trade policies and highlight the critical need for strategic adaptation in an increasingly interconnected world.

As artificial intelligence rapidly transforms industries worldwide, a prominent technology hub is striving to overhaul its infrastructure to remain at the forefront of innovation. However, this ambitious upgrade faces unexpected hurdles due to tariffs imposed during the Trump administration, which have raised costs on critical components and equipment. The intersection of cutting-edge technological advancement and geopolitical trade policies underscores the complex challenges tech centers now confront in navigating global supply chains while pursuing the future of artificial intelligence.

Tech Hub Faces Rising Costs Amid New Tariff Policies

The recent imposition of tariffs has significantly disrupted the economic landscape of one of the nation’s most promising technology hubs. Companies investing heavily in advanced artificial intelligence initiatives are now grappling with increased costs on imported semiconductor components and specialized hardware. These added expenses threaten to slow down critical research and development projects, forcing startups and established firms alike to reconsider their expansion plans or delay product launches.

Supply chain delays as companies seek alternative suppliers

Potential relocation of some production overseas to avoid tariffs

Category

Pre-Tariff Cost

Post-Tariff Cost

Increase (%)

Semiconductor Chips

$120

$156

30%

Specialized Hardware

$300

$390

30%

Assembly Components

$80

$104

30%

Impact of Tariffs on A.I. Infrastructure Expansion and Innovation

The imposition of tariffs under the Trump administration has created significant hurdles for technology hubs aiming to scale their artificial intelligence infrastructure. Import tariffs on semiconductor components, GPUs, and specialized AI hardware have escalated costs by nearly 25% to 35%, slowing acquisition timelines and driving companies to reconsider expansion strategies. This strain is particularly felt in regions that rely heavily on imported hardware to maintain competitiveness, forcing a costly trade-off between innovation pace and budget constraints.

Beyond direct pricing impacts, these tariffs have ripple effects on innovation ecosystems. Rising equipment costs limit startups’ and research institutions’ access to cutting-edge technology critical for AI breakthroughs. Key challenges include:

Delayed deployment of high-performance computing centers

Reduced collaboration due to uncertainty in supply chains

Increased investment risks leading to cautious venture funding

Component

Tariff Rate

Impact

Semiconductors

25%

Cost increase, supply delays

AI GPUs

30%

Reduced availability

Data Center Hardware

20%

Scaling bottlenecks

Strategies for Navigating Trade Barriers in the Race for Technological Leadership

Businesses and governments in emerging tech hubs are employing a mix of creative strategies to circumvent the weight of tariffs that threaten to slow their progress. Diversifying supply chains has become a top priority, with firms sourcing components from multiple countries to avoid dependency on tariff-heavy imports. Simultaneously, investments in domestic manufacturing capacity are accelerating, seeking to localize critical production stages. This dual approach not only mitigates immediate cost pressures but also enhances long-term resilience in the face of volatile trade policies.

To navigate this complex landscape, key players are also leveraging international trade agreements and diplomatic channels to negotiate exemptions or reductions on essential technologies. Collaborative R&D initiatives across borders provide alternative pathways to access advanced materials without triggering tariff penalties. Below is a snapshot of practical tactics currently in use:

Re-routing supply chains through tariff-free regions

Investing in in-country component manufacturing to reduce import reliance

Pursuing legal challenges and tariff exemptions via trade authorities

Pooling innovation resources with international partners

Strategy

Benefit

Challenge

Diversified Sourcing

Reduced Tariff Exposure

Complex Supply Logistics

Domestic Manufacturing

Control & Security

High Capital Investment

Trade Negotiations

Potential Cost Relief

Time-consuming Processes

International R&D

Access to Innovation

IP and Coordination Risks

Concluding Remarks

As the tech hub grapples with the unintended consequences of trade policies, the intersection of innovation and geopolitics grows increasingly complex. While local leaders and industry experts advocate for strategies to mitigate the impact of tariffs, the path forward remains uncertain. How this evolving landscape will shape the future of A.I. development and economic competitiveness in the region is a story still unfolding.

Kazakhstan is rapidly positioning itself as a pivotal hub in global logistics, leveraging its strategic location along the Middle Corridor to drive unprecedented transit growth. As international trade routes evolve, the Central Asian nation is capitalizing on unique geopolitical advantages to enhance connectivity between Asia and Europe. Recent figures highlight record increases in cargo volumes passing through Kazakhstan, underscoring its rising significance in the global supply chain. This surge not only cements Kazakhstan’s role as a critical transit country but also signals a broader shift in logistics dynamics-one that could reshape trade patterns and economic landscapes across continents.

Kazakhstan Emerges as a Critical Hub in the Middle Corridor Boosting Global Trade Flows

Kazakhstan has solidified its role as a pivotal junction in the Middle Corridor, a vital trade route connecting Asia and Europe. Recent infrastructure investments and streamlined customs procedures have propelled the nation’s transit capacity to unprecedented levels, making it an indispensable conduit for cargo movement. This expansion is not only enhancing Kazakhstan’s logistical capabilities but also significantly reducing transit times, offering a competitive alternative to traditional maritime routes. With enhanced rail connectivity and upgraded multimodal hubs, the country is effectively bridging gaps between major global markets, facilitating smoother and faster trade flows.

Key factors contributing to this surge include:

Modernized Rail Networks that increase capacity and reliability.

Expanded Customs Facilities enabling swift clearance and minimal delays.

Strategic Collaborations with neighboring countries to promote seamless border transit.

Investment in Digital Logistics Platforms boosting transparency and efficiency.

Below is a snapshot of Kazakhstan’s transit growth over the past three years, illustrating the rapid acceleration in freight volumes:

Year

Transit Volume (million tons)

Growth Rate (%)

2021

18.3

–

2022

24.7

35%

2023

31.5

28%

Record Transit Growth Signals Kazakhstan’s Rising Influence in Eurasian Logistics Networks

Kazakhstan’s strategic investments in its logistics infrastructure have propelled the country to the forefront of Eurasian transport corridors, showcasing an impressive increase in transit volumes over recent years. Anchored by the Middle Corridor-the vital link connecting China with Europe while bypassing Russia-Kazakhstan is rapidly becoming a hub for international freight movement. This growth is not only a testament to the nation’s geographical advantage but also a result of its modernization efforts in rail, road, and customs services, which have significantly cut transit times and costs for shippers.

Key factors driving this unprecedented rise include:

Customs reforms: Streamlined procedures reducing bottlenecks at border crossings.

Public-private partnerships: Joint ventures accelerating infrastructure upgrades and service quality.

The following table highlights Kazakhstan’s transit growth compared to neighboring countries over the past three years:

Year

Kazakhstan Transit Volume (Million Tons)

Uzbekistan Transit Volume (Million Tons)

Kyrgyzstan Transit Volume (Million Tons)

2021

45

18

12

2022

57

22

15

2023

72

25

17

Strategic Recommendations for Maximizing Kazakhstan’s Potential in the Competitive Global Supply Chain

Enhancing Infrastructure and Digital Integration: To fully harness Kazakhstan’s strategic location in the Middle Corridor, it is imperative to invest heavily in multimodal infrastructure upgrades. Prioritizing the modernization of railways, road networks, and customs facilities will facilitate smoother cargo flows and reduce bottlenecks. Additionally, implementing cutting-edge digital logistics platforms and blockchain technology can foster transparency and efficiency across the supply chain. These advancements will not only attract global freight operators but also elevate Kazakhstan as a logistics hub connecting East and West with unprecedented reliability.

Policy Reforms and International Collaborations: Streamlined customs procedures and harmonized regulatory frameworks are crucial to sustaining record transit growth. Kazakhstan can amplify its competitive edge by fostering public-private partnerships and forging alliances with neighboring countries and major trade blocs. Focused efforts on sustainable logistics practices, including green corridors and carbon footprint reduction, will align the nation with global trade priorities. The following table outlines key strategic recommendations that could accelerate Kazakhstan’s supply chain prominence:

Strategic Focus

Expected Impact

Infrastructure modernization

Reduced transit times, increased capacity

Digital supply chain platforms

Real-time tracking, enhanced transparency

Customs procedure reforms

Simplified border transit, reduced delays

Regional trade partnerships

In Summary

As Kazakhstan continues to leverage its strategic location within the Middle Corridor, the nation is solidifying its role as a pivotal hub in global logistics networks. With record transit growth highlighting the success of its infrastructure investments and international partnerships, Kazakhstan is not only enhancing regional connectivity but also reshaping the dynamics of Eurasian trade routes. Moving forward, sustained focus on innovation and expanded cooperation will be crucial for Kazakhstan’s ambitions to maintain and extend its influence on the global logistics stage.

India’s drive to become a global technology powerhouse has received a significant lift as Apple expands its manufacturing footprint in the country, benefiting from recent shifts in US tariff policies. This strategic alignment underscores India’s ambition to position itself as a key player in the high-tech manufacturing sector, leveraging both domestic initiatives and international trade dynamics. As Apple scales up production locally, the interplay between governmental incentives and tariff structures is reshaping the technology landscape, with far-reaching implications for global supply chains and India’s economic growth.

India’s Strategic Push to Become a Global Tech Hub Accelerated by Apple Investments

India’s ambition to emerge as a preeminent global technology hub is gaining unprecedented momentum as significant investments from Apple take center stage. The tech giant’s increased manufacturing footprint in India is not only a testament to the country’s improving infrastructure and skilled workforce but also a strategic move influenced by the ongoing US tariffs on Chinese imports. Apple’s pivot to India includes expanding assembly plants and investing in local supply chains, which is catalyzing job creation and innovation within the domestic electronics sector.

Key factors driving this transformation include:

Tariff Advantages: Diversifying production away from China helps Apple mitigate tariff impacts imposed by the US government.

Government Initiatives: Programs like ‘Make in India’ and incentives for electronics manufacturing boost corporate confidence.

Skilled Talent Pool: India’s expanding ecosystem of engineers and developers supports cutting-edge product development locally.

Local Supplier Development: Strengthening India’s component manufacturing to reduce dependency on imports.

Investment Aspect

Impact

Manufacturing Plants

Creation of 100,000+ jobs by 2025

Local Component Sourcing

Increased from 20% to 45% in 3 years

R&D Initiatives

Launch of 3 new innovation centers

Impact of US Tariffs on India’s Manufacturing Sector and Export Competitiveness

Recent US tariffs have inadvertently catalyzed growth within India’s manufacturing sector, especially in the high-tech arena. As Apple shifts more production to India to sidestep the increased costs from tariffs imposed on Chinese imports, local factories are undergoing rapid modernization, acquiring advanced machinery, and adopting global best practices. This infusion of technology and capital has significantly enhanced India’s capacity to produce sophisticated electronics, fostering a more resilient and diversified industrial base.

Key factors contributing to this shift include:

Increased foreign direct investment driven by multinational companies seeking tariff-free exports to the US.

Government incentives aligned with India’s Make in India initiative, accelerating infrastructural improvements.

Skill development programs tailored to meet the demands of high-tech manufacturing.

Sector

Growth in Production (%)

Export Competitiveness

Smartphone Assembly

27

High

Semiconductors

15

Moderate

Electronic Components

22

High

While India’s export competitiveness strengthens While India’s export competitiveness strengthens notably in smartphone assembly and electronic components, semiconductors are exhibiting moderate growth, indicating room for further development in complex manufacturing processes. The combined effect of increased foreign direct investment, government support, and skill development is creating a robust environment for sustained expansion in the high-tech manufacturing sector. This evolving industrial landscape positions India as a promising alternative to traditional manufacturing hubs, potentially reshaping global supply chains in the years ahead.

Policy Recommendations to Sustain Momentum and Foster Local Tech Innovation

To capitalize on the recent momentum sparked by Apple’s expanded manufacturing footprint and evolving US tariff policies, policymakers must prioritize a multifaceted approach that strengthens local innovation ecosystems. Crucially, increasing funding for startup incubators and accelerators can nurture homegrown talent, enabling Indian tech entrepreneurs to compete on a global scale. Additionally, reforming intellectual property laws to provide faster protections without compromising international agreements will incentivize creators and investors alike. Cross-sector collaboration between government, academia, and private industry should be institutionalized, fostering an environment where cutting-edge research seamlessly translates into commercially viable products.

Key recommendations include:

Implement targeted tax incentives for companies investing in R&D within India

Enhance digital infrastructure in Tier 2 and Tier 3 cities to decentralize innovation hubs

Streamline regulatory approvals to reduce time-to-market for emerging tech solutions

Facilitate public-private partnerships focused on skill development in AI, semiconductor design, and advanced manufacturing

Policy Focus

Expected Impact

Timeline

R&D Tax Incentives

Boost domestic innovation investment by 25%

1-2 years

Digital Infrastructure Expansion

Increase tech startup formation in non-metro regions

3-5 years

Regulatory Streamlining

Reduce compliance delays by 40%

1 year

Public-Private Skill Partnerships

Improve workforce readiness in emerging tech fields by 30%

2-3 years

Closing Remarks

As India positions itself at the forefront of the global technology landscape, the collaboration with Apple and the recalibration of US tariffs signal a significant milestone in the country’s high-tech ambitions. These developments not only promise to enhance India’s manufacturing capabilities and technological innovation but also reflect a broader shift in international trade dynamics. As the nation continues to attract major tech investments and navigate evolving geopolitical landscapes, the implications for India’s economic growth and its role in the global tech ecosystem will be closely watched in the coming years.

In a significant development for global trade dynamics, the recent US-China trade truce has eased tensions between the world’s two largest economies, offering a temporary reprieve for markets and businesses. However, despite progress on tariffs and broader trade barriers, a critical point of contention remains unresolved: the control and export of rare earth elements used in military applications. As both nations continue to vie for technological and strategic dominance, the unresolved rare earths issue underscores the fragile nature of the agreement and signals ongoing challenges ahead in the complex US-China relationship.

US-China Trade Truce Boosts Market Confidence but Rare Earth Military Restrictions Persist

Recent diplomatic engagements between the US and China have injected a dose of optimism into global markets, as both sides agreed to ease some trade tensions. Investors reacted positively, pushing equity benchmarks higher and stabilizing currency markets. Despite this uplift, traders remain cautious, as the talks fell short of addressing crucial restrictions affecting the rare earth minerals sector. These minerals, vital for a spectrum of high-tech and defense applications, continue to be a sticking point given their strategic military significance.

While the trade truce removes some tariffs and opens new channels for dialogue, key limitations governing the export and supply of rare earth elements used in military technologies remain firmly in place. The ongoing restrictions highlight the complexity of decoupling economic cooperation from national security concerns. Below is a summary of the current situation affecting rare earth minerals in this context:

Aspect

Status

Impact

Trade Tariffs

Partially Eased

Market Confidence Boosted

Rare Earth Exports for Civilian Use

Mostly Open

Supply Chains Stabilizing

Rare Earth Exports for Military Use

Strictly Restricted

Geopolitical Tensions Persist

US Strategy: Maintain technological edge through controlled rare earth access.

China’s Stance: Retain leverage by regulating critical mineral exports.

Market Reaction: Volatility expected until security concerns ease.

Strategic Importance of Rare Earth Elements Highlights Ongoing Security Concerns

The ongoing trade truce between the US and China has failed to adequately address the critical issue surrounding rare earth elements (REEs), which are essential for military and high-tech applications. These minerals play a pivotal role in manufacturing advanced weaponry, communication systems, and aerospace technologies, making their supply chain a strategic security matter. Despite diplomatic efforts, the heavy reliance on Chinese exports for these materials continues to expose vulnerabilities in American defense and technology sectors, fueling concerns about future access during geopolitical tensions.

Key challenges in the rare earth supply chain include:

Monopolized global production dominated by China

Limited alternative sourcing and processing capabilities in the US

Potential for export restrictions during political disputes

REE Application

Military Usage

Supply Risk Level

Neodymium

Guidance systems & magnets

High

Europium

Laser targeting & communication

Medium

Yttrium

Night vision devices

High

Policy Recommendations Urge Enhanced Supply Chain Diversification and Diplomatic Engagement

In light of ongoing tensions and supply fragility surrounding rare earth materials critical for military applications, experts are urging a multi-pronged strategy that goes beyond temporary trade agreements. Emphasizing the need to reduce dependency on single-source suppliers, policy analysts advocate for diversifying supply chains by investing in alternative mining operations, recycling technologies, and fostering partnerships with allied nations. This diversified approach is seen as essential to mitigate the risks associated with geopolitical leverage and supply bottlenecks that could jeopardize national security.

Simultaneously, there is a call for increased diplomatic engagement aimed at establishing transparency and cooperative frameworks around rare earth exports. Proposals include:

Joint research initiatives to develop substitutes and recycling innovations

Strategic dialogues to reduce the weaponization of rare earth supply chains

Policy Focus

Proposed Action

Expected Outcome

Supply Chain Resilience

Expand mining & recycling

Reduced reliance on single sources

Diplomatic Cooperation

Establish multilateral frameworks

Greater trade transparency & security

Technological Innovation

Invest in rare earth alternatives

Minimized strategic vulnerabilities

The Conclusion

While the recent US-China trade truce offers a temporary easing of economic tensions, the critical issue of rare earth minerals for military applications remains unaddressed. As both nations continue to vie for technological and strategic supremacy, experts warn that the unresolved supply chain vulnerabilities could pose significant risks to national security. Stakeholders and policymakers alike will be closely monitoring future negotiations to see if concrete measures emerge to safeguard these essential resources amid a shifting geopolitical landscape.

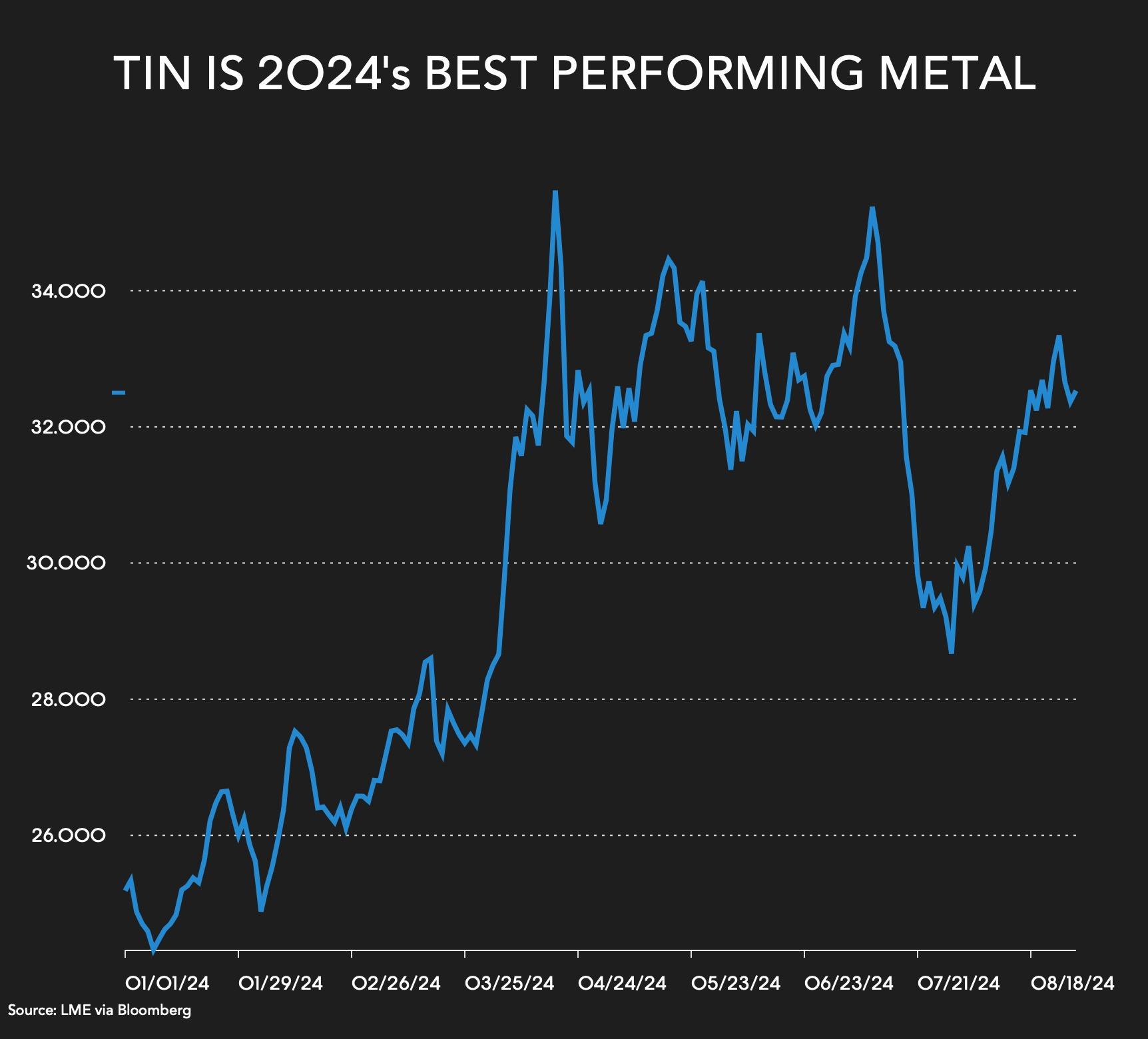

Tin prices surged to a one-week high amid growing concerns over the sluggish restart of supply from Myanmar’s Wa State, a key source for the metal. Market participants reacted to reports of ongoing logistical challenges and production delays, fueling uncertainty about global tin availability. The supply bottleneck has intensified fears of tightening inventories, pushing traders to reevaluate short-term outlooks for this critical industrial metal.

Tin Prices Surge to One Week High Amid Supply Fears from Myanmar’s Wa State

The tin market has experienced a notable rally as traders react to ongoing disruptions in the supply chain originating from Myanmar’s Wa State. Key mining operations have faced setbacks due to logistical hurdles and political uncertainties, casting doubt on the speed at which production can resume. This constrained supply outlook has sparked concerns among investors and industrial users, pushing tin prices to a one-week high on major exchanges.

Delayed shipment schedules due to regional instability

Reduced output from local mining companies amid regulatory challenges

Growing global demand for tin in electronics and solder manufacturing

Parameter

Current Status

Wa State Mining Activity

Below 50% capacity

Tin Export Delays

Up to 3 weeks

Price Change (Last 7 days)

+5.4%

Analyzing the Impact of Myanmar’s Slow Wa State Restart on Global Tin Markets

The ongoing delays in the resumption of mining activities in Myanmar’s Wa State have sent ripples through the global tin markets, pushing prices to a one-week peak. Wa State, known for its significant contributions to the world’s tin supply, faces logistical and regulatory hurdles that have slowed down production considerably. Traders and investors are growing increasingly concerned as the constrained supply tightens market availability, fueling speculative buying and price volatility.

Key factors influencing tin prices include:

Disrupted supply chains due to extended geopolitical uncertainties

Reduced output amidst local operational challenges and security concerns

Heightened demand from electronics and automotive sectors amid global recovery

Impact Area

Effect on Tin Market

Supply

Decrease by 15-20%

Price Volatility

+8% in last 7 days

Investor Activity

Increased speculative trading

Strategic Recommendations for Traders Navigating Volatility in Tin Supply Chains

Traders must prioritize agility and diversification to effectively manage the current volatility in tin supply chains. With Myanmar’s Wa State struggling to resume full production, reliance on a single source has proven increasingly risky. Engaging with multiple supply channels and monitoring geopolitical developments can provide critical buffers against sudden disruptions. Additionally, maintaining close communication with suppliers and logistics partners will help anticipate delays, enabling more informed decision-making.

Implementing a data-driven approach to market analysis is essential during this period of uncertainty. Leveraging real-time price indicators and inventory reports allows traders to optimize entry and exit points. Below is a quick-reference guide outlining key strategies to employ:

Supply Chain Diversification: Avoid dependency on high-risk regions.

Real-Time Monitoring: Track price and shipment updates continuously.

Risk Assessment: Evaluate political and environmental factors regularly.

Inventory Management: Adjust stock levels to balance demand and supply uncertainties.

Strategy

Benefit

Recommended Action

Supply Chain Diversification

Reduced exposure to single-region risk

Identify alternative suppliers in stable regions

Real-Time Monitoring

Improved responsiveness to market moves

Use live tracking tools and price alerts

Risk Assessment

Early identification of potential disruptions

Conduct periodic geopolitical analysis

Inventory Management

Balanced holding costs with market demand

Adjust inventory to buffer supply shocks

Insights and Conclusions

As concerns linger over the slow restart of tin supply from Myanmar’s Wa State, the metal has reached a one-week high, underscoring the market’s sensitivity to geopolitical and logistical disruptions. Industry stakeholders will be closely monitoring developments in the region, as sustained supply constraints could continue to impact tin prices and global supply chains in the weeks ahead.

Evaluating Taiwan’s Weaknesses: The Threat of Systemic Breakdown

An insightful report published by the South China Morning Post has raised concerns regarding Taiwan’s susceptibility to a catastrophic systems failure that could incapacitate the island without any direct military confrontation. Findings from a military journal indicate that vulnerabilities in Taiwan’s critical infrastructure and cybersecurity measures could be exploited to disrupt essential services and communication networks. This disruption would severely hinder the nation’s ability to respond effectively during escalating crises. Such emerging threats underscore growing concerns about asymmetric warfare strategies amid ongoing regional security challenges.

Grasping Systemic Breakdown and Its Repercussions on Taiwanese Defense

The dangers confronting Taiwan extend far beyond traditional combat scenarios.Analysts warn that a systemic collapse—triggered by cyberattacks, economic turmoil, or failures in infrastructure—could immobilize the island’s defenses even before hostilities begin. These situations would exploit Taiwan’s highly interconnected society where vital infrastructures such as power grids, communication systems, and financial networks are crucial for both civilian life and military readiness. The military publication stresses that compromising these systems can substantially weaken Taiwan’s defensive capabilities, rendering its advanced weaponry and strategic alliances ineffective.

As a result, defense planners must prioritize enhancing resilience across multiple sectors to counter these unconventional threats. This includes bolstering cybersecurity measures, establishing decentralized command structures, and investing in backup systems designed to ensure operational continuity under duress. Below is an overview of meaningful vulnerabilities along with suggested strategic responses:

Communication Systems

Infrastructure Component

Weaknesses Identified

Proposed Defense Strategies

Power Grid

Sensitive to targeted cyber intrusions.

Implement grid segmentation along with rapid isolation protocols.

Centralized networks vulnerable to disruptions.

A thorough multi-domain resilience strategy is vital as part of national defense planning.

Civil-military cooperation is essential for effective risk management.

Regular scenario-based training will improve readiness for fast responses during cascading failures.

Infrastructure Vulnerabilities Highlighted by Military Research

A recent inquiry has spotlighted critical weaknesses within Taiwan’s infrastructure that could lead to incapacitation without conventional military action. Essential services such as electricity supply chains, water management facilities, and telecommunication networks have been identified as vulnerable targets; simultaneous disruptions could trigger widespread chaos.Analysts caution that such multifaceted failures jeopardize governmental operations while undermining emergency response effectiveness—essentially neutralizing defensive capabilities before any physical conflict arises.

The report underscored several key points of vulnerability:

Main power distribution centers: at risk from both cyberattacks or physical sabotage;