This week, Polypropylene prices slipped in South Asia while remaining steady in the Far East Asian and Southeast Asian region.

An industry source in Asia on condition of anonymity informed a Polymerupdate team member, “The rising possibility of a retaliatory strike by Iran and its proxies against Israel has raised the risk of oil supply disruptions from the Middle East, exerting a bullish pressure on crude oil prices. However, market observers stated that the overall market sentiment continued to remain weak, with a rise noted in US gasoline inventories, signalling dampened demand for fuel products.”

In India, PP raffia and PP injection prices were assessed at the USD 990-1030/mt CFR levels, both down USD (-30/mt) from the previous week. PP film and BOPP prices were assessed at the USD 1010-1050/mt CFR levels, both week on week declined by USD (-30/mt). PP block copolymer prices were assessed at the USD 1030-1070/mt CFR levels, a fall of USD (-30/mt) from the previous week.

In India, Middle Eastern producers offered their PP raffia and Injection grades in the range of USD 990-1030/mt CFR levels, for shipment in August 2024.

In India, the regional purchase pulse was reportedly muted with traders selling material below prices quoted by producers. Buyers are holding back from making additional purchases as they are already holding additional inventories, indicating weak demand amid the monsoon season. Meanwhile, Nayara Energy has commenced production at a 450,000 mt/year PP plant in Vadinar, Gujarat last week. With the producer offering off-spec grade material to Indian buyers, participants are anticipating an influx of material in the market, possibly lowering the purchase appetite for PP import cargoes next year. Furthermore, domestic producers made scheme announcements to spur buying activity.

In Pakistan, PP raffia and PP injection grade prices were assessed at the USD 1040-1070/mt levels, both lower by USD (-30/mt) from the previous week. PP film and BOPP prices were assessed at the USD 1060-1100/mt CFR levels, both week on week decreased by USD (-30/mt). PP block copolymer prices were assessed at the USD 1070-1130/mt CFR levels, down USD (-30/mt) from last week.

In Pakistan, Middle Eastern producers offered their PP raffia and Injection grades in the range of USD 1040-1070/mt CFR levels, for shipment in August 2024.

In Pakistan, a sluggish purchase pulse coupled with lower import offers from overseas suppliers supported the price drop. Buyers in the country are heard to have adopted a wait and watch approach and are currently refraining from engaging in transactions as they continue to track developments in the markets of neighbouring countries.

In Sri Lanka, PP raffia and PP injection grade prices were assessed at the USD 1050-1090/mt CFR levels, both sharply down USD (-40/mt) from the previous week. PP film and BOPP prices were assessed at the USD 1090-1120/mt CFR levels, both week on week lower by USD (-40/mt). PP block copolymer prices were assessed at the USD 1110-1130/mt CFR levels, a slide of USD (-40/mt) from the previous week.

In Sri Lanka, Middle Eastern producers offered their PP raffia and Injection grades in the range of USD 1050-1090/mt CFR levels, for shipment in August 2024.

In Sri Lanka, new offers, which have been announced by overseas suppliers, are revised lower as compared to previous offer levels. The upcoming presidential election in the island nation next month could weigh on buying appetite.

In Bangladesh, PP raffia and PP injection prices were assessed at the USD 1040-1070/mt CFR levels, both declined by USD (-30/mt) from the previous week. PP film and BOPP prices were assessed at the USD 1060-1090/mt CFR levels, both week on week lower by USD (-30/mt) . PP block copolymer prices were assessed at the USD 1100-1150/mt CFR levels, a fall of USD (-30/mt) from last week.

In Bangladesh, Middle Eastern producers offered their PP raffia and Injection grades in the range of USD 1040-1070/mt CFR levels, for shipment in August 2024.

In Bangladesh, offers were limited with minimal buying activity seen in the region. An uncertain political environment in the country has further dampened market sentiment.

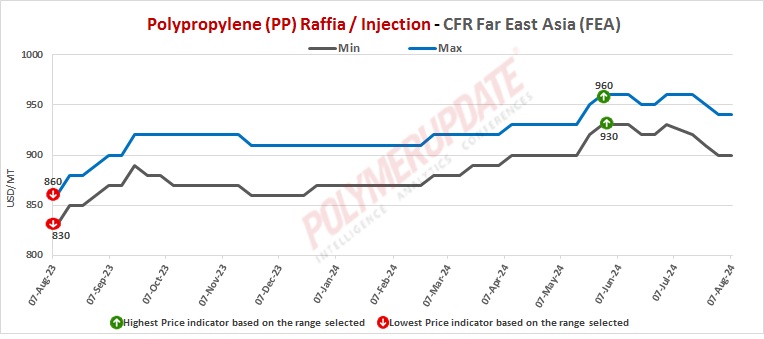

Meanwhile, in Far East Asia, PP raffia and PP injection prices were assessed at the USD 900-940/mt CFR levels, both rolled over week on week. PP film and BOPP prices were assessed flat at the USD 910-950/mt CFR levels. PP block copolymer prices were also assessed steady at the USD 930-960/mt CFR levels.

In China, supply turned surplus as a few production facilities concluded their maintenance. A combination of weak demand and ample supply prompted overseas suppliers to lower their offers to China. Meanwhile, logistical bottlenecks in certain regions drove a few Middle Eastern suppliers to increase their exports to China. Although reduction in freight rates bolstered export activity, demand in export markets has not experienced a significant pickup.

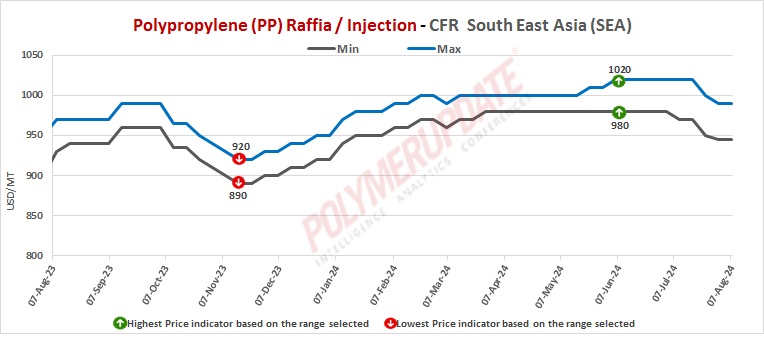

In Southeast Asia, PP raffia and PP injection grade prices were assessed flat at the USD 945-990/mt CFR levels. PP film and BOPP prices were assessed at the USD 955-1000/mt CFR levels, both stable week on week. PP block copolymer prices were assessed at the USD 980-1020/mt CFR levels, constant from the previous week.

In Southeast Asia, competitively-priced cargoes of ASEAN origin, especially comprising flat yarn and injection grades, continued to weigh on PP prices. In Indonesia, the attempts by some local suppliers to raise domestic offers was met with a lack of enthusiasm from buyers, reflecting a weak purchase pulse in the region. A few converters continued to track the current freight rate movement, anticipating a further decline in rates in the later part of August. Regional cargo availability is likely to increase with some plants raising their output levels while other are expected to restart operations soon.

Feedstock propylene prices on Tuesday were assessed at the USD 865-875/mt CFR China levels while FOB Korea propylene prices were assessed at the USD 845-855/mt levels, both unchanged week on week.

In plant news, Formosa Plastics Corp has shut down its No.2 Polypropylene (PP) unit on August 5, 2024. Further details on the duration of the shutdown could not be ascertained.” Located in Ningbo, Zhejiang in China, the No.2 unit has a production capacity of 280,000 mt/year.

In other plant news, PetroChina Ningxia Petrochemical is likely to restart its polypropylene (PP) unit in September 2024. The plant was shut for maintenance on July 3, 2024.

Located in Yinchuan, China, the PP unit has a production capacity of 110,000 mt/year.

In another plant news, OQ has taken off stream its No.1 and No.2 Polypropylene (PP) units in end July 2024. Further details on the duration of the shutdown could not be ascertained. Located in Sohar, Oman, the No.1 and No.2 units have a production capacity of 170,000 mt/year each.

Source link : http://www.bing.com/news/apiclick.aspx?ref=FexRss&aid=&tid=66b37e5327e54a83a8ffad5db374705a&url=https%3A%2F%2Fpolymerupdate.com%2FNews%2FDetails%2F1328269&c=7836885481698823868&mkt=en-us

Author :

Publish date : 2024-08-06 21:30:00

Copyright for syndicated content belongs to the linked Source.

{kind=link}